The Hidden Risks Behind Beijing’s New Monetary Moves

China’s real estate crisis since 2021 still lingers, and US tariffs continue to pressure its economy. In response, Beijing’s new monetary policies aim to shield growth but may unintentionally worsen the situation. Could these moves backfire and deepen China’s economic challenges?

ECONOMICSCHINAMACRO ECONOMYGLOBAL NEWSMONETORY POLICY

Nagaraj Basarkod

5/22/20252 min read

The tariff war launched by Donald Trump sent shockwaves through global markets, rattling economists and policymakers alike. The US Federal Reserve opted for caution, maintaining its policy stance amid the unpredictability of "Trumponomics." For much of the world, however, this trade standoff was a wake-up call—prompting nations to seek self-reliance and diversify their trade partnerships.

To shield their economies from trade war fallout, central banks around the world began slashing interest rates. The European Central Bank cut rates by 25 basis points for the third consecutive time this year, while the Reserve Bank of India lowered rates by 50 basis points. Traditionally, high uncertainty calls for higher rates to offset lending risks, making this wave of rate cuts appear counterintuitive at first glance. Know the rationale of rate cuts amid trade war in the context of india.

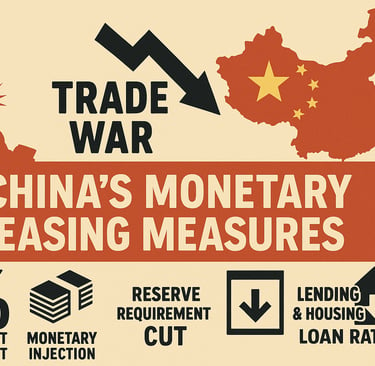

China, meanwhile, not only retaliated against US tariffs but also doubled down on efforts to boost its domestic economy. The People’s Bank of China (PBOC) has rolled out a series of monetary easing measures—injecting $138 billion into the economy, trimming the repo rate by 0.1%, cutting the reserve requirement ratio by 0.5%, and reducing long-term lending and housing loan rates by 0.25%. The reserve requirement for financial leasing and vehicle financing companies was even eliminated, freeing up more funds for lending.

These aggressive moves come as China’s real estate crisis, triggered by the collapse of Evergrande and other overleveraged developers, continues to drag on. Despite repeated stimulus efforts, new home prices have stagnated for nearly two years, with April 2025 seeing a 4% year-on-year drop. Property investment has fallen sharply, and confidence in the sector remains weak as indebted developers struggle to deliver pre-sold homes.

China’s vast industrial capacity—an asset in boom times—has become a liability amid weak domestic demand and an aging population. The government’s push to boost local consumption faces cultural and demographic headwinds: Chinese households save much of their income, with consumption accounting for just 40% of GDP. Simply making credit cheaper may not spur spending; much of the liquidity could end up back in savings or channeled into further industrial expansion, exacerbating overcapacity.

Moreover, China’s reliance on debt-fueled stimulus is raising alarm bells among global ratings agencies. Fitch recently downgraded China’s credit rating, citing surging government debt and persistent real estate woes as major vulnerabilities. The government deficit is forecast to hit 8.4% of GDP in 2025, far above the median for comparable economies.

In short, while China’s rate cuts are designed to revive growth and stabilize the property market, they risk fueling new imbalances—encouraging risky lending, deepening industrial overcapacity, and potentially undermining financial stability. The world is watching to see whether Beijing’s bold monetary experiment will deliver a turnaround, or set the stage for even greater challenges ahead.

Contact

+91 - 9738482563

© 2025. All rights reserved.

nagaraj.basarkod@yahoo.in