Microservices: A Strategic Imperative for Financial Services

How microservices are reshaping the financial services industry. From building trust and ensuring availability to improving speed, scalability, and compliance, it explains why microservices are no longer just a tech choice but a strategic need for banks and financial institutions

MICROSERVICESSTRATEGYFINTECHFINANCIAL SERVICES

Nagaraj Basarkod

9/16/20255 min read

Finance is as old as human civilisation, built on a single attribute: trust and every financial innovation, from coins to digital wallets, has relied on maintaining this trust. Any financial institution or service fails to meet this basic need is bound to fail in no time.

As the number of people who transact increases, the need for a market, players facilitating the transactions and innovations to lure the transactors increase. The scale of transactions and innovations lead to loopholes leading to fraudulent activities and stricter governance and regulations.

Few of the great abilities of the tech that I personally appreciate are agility, scalability, and the pace of execution. But large and complex systems with tangled modules and intertwined logic reduces the agility to adopt for changes, support innovations and scale without compromising on the pace of execution. Such complex systems pose a threat of one point failure and susceptible to hacking and data breaches.

Micro-services come handy in tackling the limitations to an extent, let’s dive-in to understand more about micro services and their role in financial services.

Microservices

These are smaller modules, developed and deployed independently, that together form the building blocks of a larger system.

Such systems have decentralised responsibilities across the modules, with greater agility and meet the functional needs of the larger system without adding to complexity.

Attributes of finance software system

Trust - Security is of prime importance

System should be trustworthy, financial services hold the crucial and confidential information of the Individuals and their transaction details.

Micro-services are designed to stay independent, it can be designed such that, internal modules have strict TLS to make the connections secure. Because of their distributed nature, micro-services make it harder to breach the entire system. A compromised service can be isolated, containing risk.

Scale - Should adopt for spike in transactions

System should accommodate the spike in the number of requests it receives and serve the client without compromising on the availability, speed, security, consistency and accuracy.

Micro-services can be scaled individually without having to scale the entire system, based on which service is most utilized today or projected to be in demand (using data and AI for prediction).

Availability - Should be up and running

In the connected global economy, no financial institution can afford to display ‘Under maintenance’ and suspend services. Customers expect uninterrupted and reliable service in realtime.

Micro-services will let you run upgradation, bug fixes and maintenance on individual services without having to shutdown and redeploy the whole system.

Agile - Should be innovation friendly

Finance is one of the fast growing sectors, the system should be agile enough to adopt for the innovations, quick updates/fixes, and fail fast or scale fast.

Micro-service architecture, individual teams own a service unlike in a monoliths. Teams do not need to know the internals of other systems, since services are loosely coupled and interact via APIs. Each service can pick its own tech stack, pace of development, versioning and time of deployment.

Governance - Should adopt for changing regulations

Finance is highly regulated with little room for out of the box innovations considering its sensitivity and adverse impact on economy if not managed well.

Micro-services can be updated frequently to adjust for the changing governance without having to impact the whole system. Modular compliance enables institutions to adapt faster to new laws, turning regulation into a competitive differentiator. If there is regulatory change with KYC, only that service will be modified and deployed. As interactions between services happen over the API, its possible to design auditable facade APIs that not only improve transparency but also simplify regulatory reporting and compliance audits.

Speed - Should be quick and real-time

The days of money orders are long gone. Customers now expect instant transactions, operating on a principle of zero trust. Transaction speed directly shapes customer confidence. Every additional second increases anxiety and erodes trust.

In today's fast paced world, micro-services help the system to asynchronously distribute the work among multiple services. A simple payment system involves multiple checks and nodes to connect along with query for fraudulent transactions, notifications and many more.

Challenges

Building the system with micro-services is not as simple as sounds on the document, it comes with its own challenges and costs.

Orchestration

It’s difficult to let individual teams work in silos and yet keep them under the same umbrella. It requires strong interpersonal skills and technical empathy balancing the needs of multiple teams while driving toward shared outcomes. Every team strives for the best outcomes within their service, and this energy must be channeled into delivering a robust system overall. Successful adoption requires strong interpersonal skills, technical empathy, and leadership that fosters collaboration, ownership, and accountability across teams.

Integration

Micro-services might work the best in silos, but, the reality check is when they are integrated into the system. Each micro-service must go through stringent TDD and should be tested for integration. That’s where CI/CD pipelines take their precedence. One cannot let the loose ends get integrated into the system.

Data consistency

Often micro-services use their own databases and its crucial to keep the data in sync across the data bases and caches. The system must be able to retrieve the updated info consistently without lag. Consistent and updated info is crucial for banking systems.

Security

In finance, every endpoint is a potential risk. System works on the principle of Zero Trust, API gateways have to equipped with authentication services and inter service communication has to be verified and protected. Securing APIs, managing encryption, and ensuring auditability are non-negotiable.

Leveraging the micro-service architecture

Maximising the value for its stakeholders is the core of any business. Lets see how we can leverage the micro-services architecture in banking system other than architecture or refactoring.

Enhanced customer experience

Micro-services help the tech to break free from the legacy monoliths exposing the facade APIs with higher level of security and just the right amount of relevant information. Financial service institutions can leverage this to make user interfaces simpler and interactive. Provide multiple channel access to banking. ex: YONO SBI

Performance enhancement at every stage

Monoliths often make it difficult to break down the API performance among multiple activities, making it difficult to track down the bottle neck in the process. Often its difficult to pin point to root and take necessary actions. Micro-services are loosely coupled, one can easily track all the intermediate APIs to know which is the bottleneck and work on resolving it.

Innovations

In order to make innovations flourish, the team should have sufficient elbow room and decision making abilities and free from regulatory, at least till a POC is reached. The major concern many orgs face is the access to their system, often innovations are discouraged considering the sensitive data and the responsibility they own. With micro-services, you can isolate the team and give the limited / selected access to their service, protecting the main system intact. ex: UPI over the existing banking services.

3rd Party Integrations

Micro-services make 3rd party integrations easy and simple. When an organisation can be anything, its best if it focuses on its vision and mission instead of trying to do everything. Micro-services open the door for banks to partner seamlessly with fintechs, loyalty platforms and many more solutions, expanding ecosystems, unlocking new revenue streams, and strengthening customer loyalty while maintaining security. ex: E-Com websites integrating payments

API as a source of revenue

Banking as a Service, where a banking system exposes the APIs letting the developers leverage the core functionalities without having to start something from scratch. This helps banks to attract the tech savvy customers without having to put much of efforts. Banks can leverage on the data by the 3rd party integrators to know their customers better.

In day-to-day banking interactions, systems are exposed to countless APIs and third-party interfaces. Each of these connections represents both an opportunity to expand services and improve customer experience and a risk, as every interface must be governed, secured, and audited. Micro-services make it possible to manage these integrations with greater agility, turning what was once a source of complexity into a driver of innovation.

Micro-services are more than an architectural shift; they are a strategic enabler for modern finance. They empower institutions to adapt to regulation, deliver always-on services, scale with demand, and innovate continuously. For customers, this translates into speed, reliability, and trust. For institutions, it brings efficiency, resilience, and competitive strength. As financial services evolve, those who align technology choices with business priorities will shape not just the systems of tomorrow, but the very future of finance.

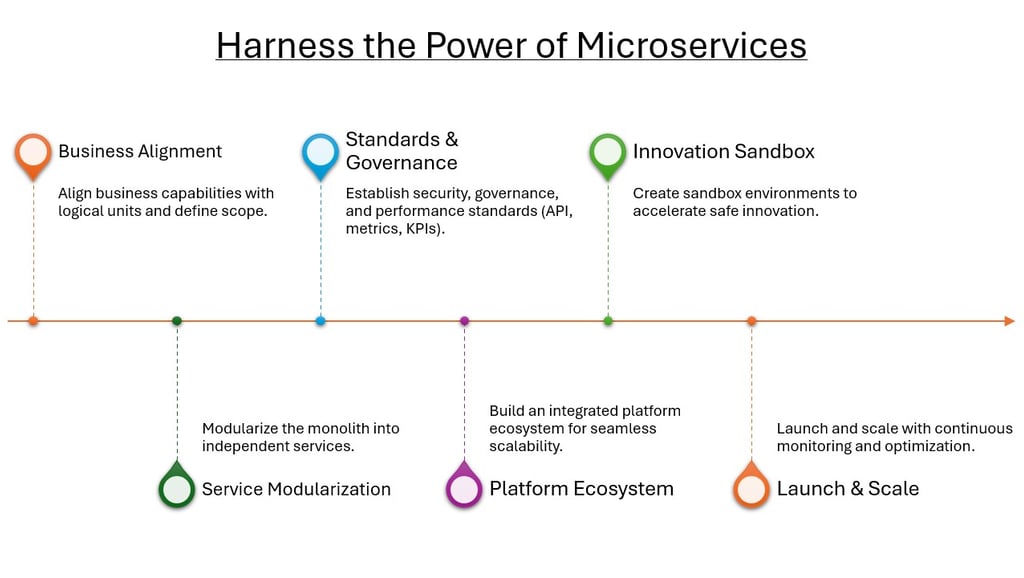

Roadmap

Contact

+91 - 9738482563

© 2025. All rights reserved.

nagaraj.basarkod@yahoo.in